The Magic of Compound Interest

Let us imagine it is 1 September and we invest a capital of 1 euro. Suppose this is a magical investment that allows the accumulated amount to double every day. On 2 September the capital will have grown to 2 euros (1 euro of initial capital plus 1 euro of return), on 3 September to 4 euros (2 euros of starting capital and 2 euros of return), on 4 September to 8 euros, and so on. According to this progression, how much would the capital amount to at the end of the month?

This is the magic of compound interest, or “the compounding of returns”, where the gains earned are automatically reinvested and generate new gains. Following this progression, by 30 September we would have an astonishing sum exceeding five hundred million euros – a figure that seems to defy our imagination.

Now imagine instead that we decide to withdraw the return earned at the end of each day, leaving only the initial sum invested. How much would we have accumulated by the end of the month?

This is the case of simple interest. The result feels much more familiar to our minds: at the end of the month we would have 30 euros – the original 1 euro plus the 29 euros earned from the magical investment (one euro per day for 29 days).

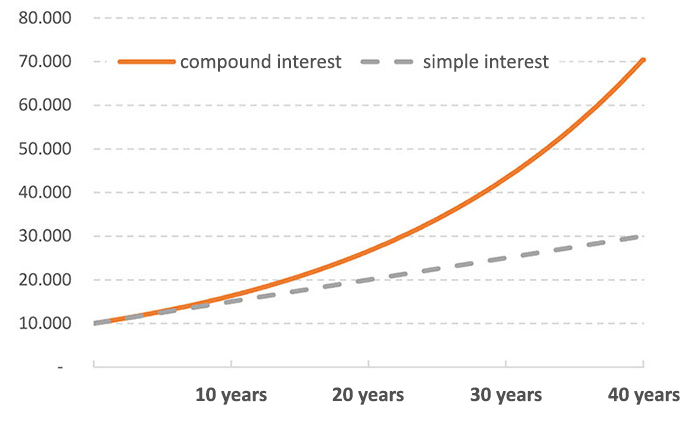

Something very similar happens with real-world investments. Thanks to our interest calculator, we can see how reinvesting returns – that is, applying compound interest over time – can radically change the final outcome of an investment, even with the same rate of return.

For example, assuming an investment of 10,000 euros at an interest rate of 5%, Figure 1 shows how the multiplying effects of compound interest become progressively more pronounced as time passes. After 40 years we would have more than 70,000 euros with compound interest, and “only” 30,000 euros with simple interest.

Fig. 1 – Growth of invested capital under the two assumptions of simple interest and compound interest

(values are expressed in euros)

"I made my first investment at age 11. I was wasting my life up until then."

With these words, Warren Buffett – the world’s most famous investor and one of the richest individuals on the planet – reminds us of the importance of compound interest when investing over long periods. Buffett is not the investor who achieved the highest annual returns, but he began investing very early. Thanks to the power of compound interest, he accumulated most of his wealth – over 90% – after turning 65. Today, at 92, he continues to invest!

A Not-So-Exponential Brain

As we have seen, people tend to underestimate the effect of compound interest – or the compounding of returns, which occurs when gains are not withdrawn but reinvested – and the exponential growth of capital that it generates. These phenomena start from very low levels and appear negligible for a long time, only to accelerate dramatically later on.

Exponential Growth: Further Examples

Imagine placing one bacterium in a bottle, and suppose it reproduces by splitting into two every minute: from two bacteria we get four, from four eight, and so on. The experiment begins at 11 a.m., and at 12 noon we discover that the bottle is full.

At what minute was the bottle half full? Just one minute before 12!

Two minutes earlier, it had been only one quarter full.

Five minutes before midday, the bottle was… just 3% full!

It took three hundred years, from 1500 to 1800, for the global population to double from 500 million to one billion; only about 120 years to double again to two billion; and just 45 years to double once more to four billion.

The Moon is on average just over 384,000 km from Earth. If we had a sheet of office paper 0.1 millimetres thick, how many times would we need to fold it for the total thickness to exceed the distance between the Earth and the Moon? Only 42 times!

Many studies have shown that people tend to underestimate the effects of exponential growth. It is as if our brains evolved to understand linear phenomena more readily than exponential ones.

This cognitive bias can significantly affect people’s lives and well-being. Research shows that individuals who underestimate long-term benefits tend to save and invest less.

Consider how important it is to begin saving and investing even small amounts for one’s retirement as early as possible, to make full use of the “magic” of compounding – given how much difference even a few additional years of investment can make. Or consider the tendency to “cash in” gains, for example annually, by selling investments or spending the returns. This shifts us back into a simple-interest scenario, which, as we have seen, is much less favourable for long-term growth.

Understanding the implications of compound interest for both investments and borrowing – and the exponential growth of capital or debt that follows – is one of the keys to managing personal finances more consciously.

RSS

RSS

E-mail Alert

E-mail Alert